There’s a belief, at least around Silicon Valley, that the so-called Millennials (those born somewhere between the years 1980 and 2000) just simply aren’t engaged at work.

This isn’t limited to startups. Companies like Google with enormous resources and brainpower are hiring “Millennial consultants” to better understand younger workers. Oracle and HBO want to stem employment churn and have made commitments to better understanding workforces in their 20s to early 30s.

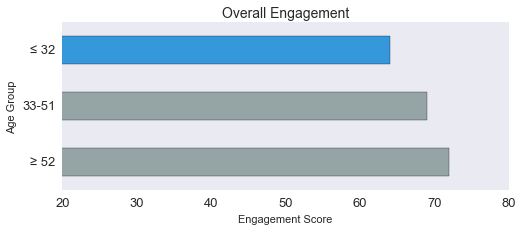

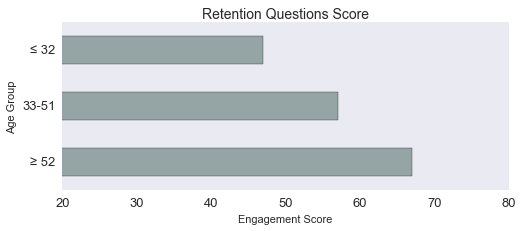

When we look at our data (specifically, our New Tech Benchmark), we see a lot of this too. Workers under 33 years of age simply have lower overall engagement than other age groups. Scores are out of a possible 100.

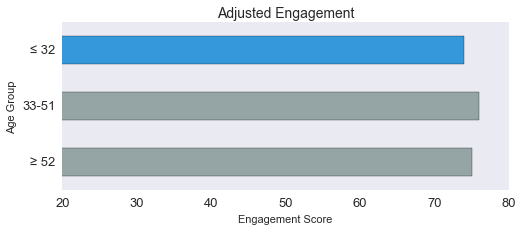

However, if we factor for the question “I see myself at Company X in two years time,” and remove its influence on the overall engagement score, the cohort under 33 years of age appear to be just as engaged as everyone else.

This effect suggests that younger workers simply have no intentions to stay at the company they work for, across the board and regardless of situation — even if they are highly engaged.

This is a big deal because retaining workers consistently ranks as a high-priority for many organizations. It’s expensive to make up for the ones you’ve lost, even for an “average” worker. Not to mention the intangible damages like morale. But why is retention seemingly so much more difficult for Millennials?

Let’s look at the data:

Workforce Development Lags Behind

Particularly in Silicon Valley, the growth of technology is outpacing the need to learn it. Hell, the speed at which technology becomes obsolete is outpacing the speed at which someone can learn it.

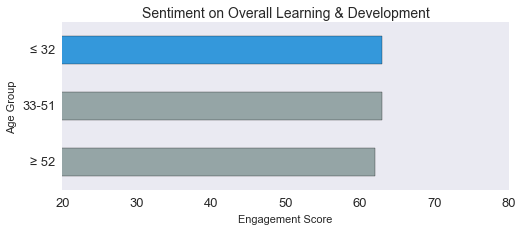

Our data show a similar trend. People at their jobs are not too happy with the level of L&D they receive. Indeed, it is one of the overall lowest scoring metrics we collect:

In the gig economy, a good way to learn new skills is to leave your current job and go to a new one. Work a job for a few years, pick up new skills, and move on to the next with new skills in-hand. Top-ranked business schools like INSEAD are teaching people to build portfolios, telling people to “switch employers and industries frequently and change paths.”

“… the training or education programs of most companies tend to fall far behind employees’ needs.“ — Quartz

And Your Value Can Double By Leaving

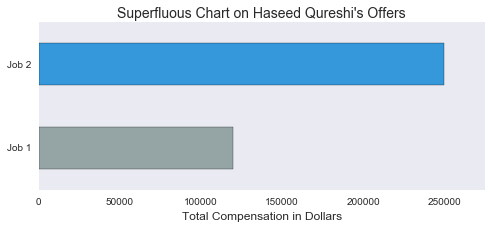

Compounding the lack of training, there were 5 million job openings in April 2016, the highest number in history. Workers are finding that their skills are increasingly more valuable not just at their job, but everywhere else, too. If employers aren’t training their staff and won’t hire people that need training, the only choice is to hire people from other companies. This quickly turn into a very expensive bidding war for talent.

The signal to employees: you must shop around constantly for a better deal, or you are leaving money on the table. In Haseed Qureshi’s case, his salary more than doubled without a single day at a job.

Take Consideration of The Long Play

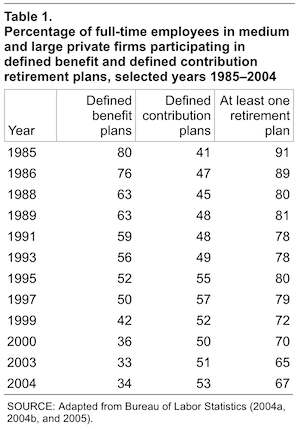

Let’s talk pensions — how many of us have them? Traditional Defined-Benefit (DB) pensions have decreased steadily at least for a couple of generations. Defined benefits are what people are usually talking about in America when they say “pension”— a guaranteed amount that’s paid out after retiring with your company — 80% of workers had these in 1985. In 20 years, or about one generation, that number has decreased to 34%.

While there are benefits to having full control of your own retirement accounts and not being tied to a job until retirement, 401ks and IRAs will only be on par with DB pensions if people put (a lot) more money into them than they are right now. And the easiest way to do that is simply to earn more. An easy way to earn more is to get a new job.

Tying it Together

There are a lot of reasons for Millennials to be fickle about the workplace. The last few decades left them with no pensions, insufficient training in the areas they need, and the rise of the gig economy. So, it comes as a bit of a surprise that companies are left asking why they can’t keep workers around by offering ping-pong tables and free beer at the price tag of $20,000 an hour.

But, there’s one giant catch: there is no evidence to suggest Millennials are leaving their jobs at a more frequent rate than previous generations.

The Problem of the Millennial Problem

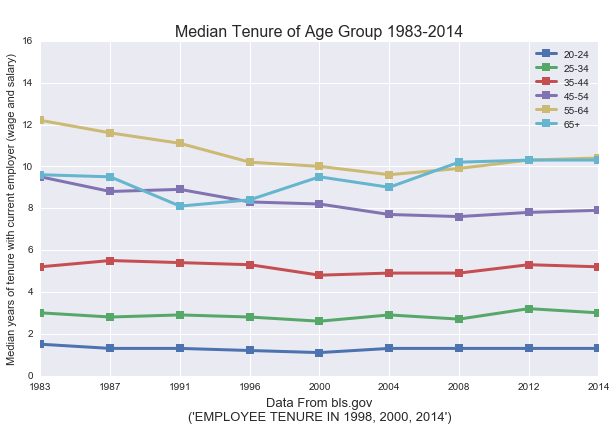

When it comes to staying at a job, Millennials are no statistically different than generations past. The U.S. Bureau of Labor Statistics’ data shows that median tenure at a job has held steady across younger workers for at least 30 years.

Older workers, of course, have longer median tenures because they’ve been in the workforce longer. But what’s interesting is how steady the increases of medians are between cohorts. Our data shows a complementary effect: older workers answer more positively on retention-related questions (i.e. I plan on staying at Company X for the next two years) in a steadily increasing manner.

The implication here is younger people simply feel less confident about their career trajectory and and grow more confident as they are more established (obvious). Simultaneously, younger workers have been staying at their jobs at a consistent rate for decades. In short, there is nothing wrong with the kids these days. They are not leaving jobs more frequently. They are just as committed, proud, and motivated as everyone else.

Our sires’ age was worse than our grandsires’. We, their sons, are more worthless than they; so in our turn we shall give the world a progeny yet more corrupt. — Horace

Though the factors stated earlier heavily coincide with the timing of Millennials entering the job market, it should be emphasized that these factors reflect the current reality of employment for everyone. Everyone cares about retirement, skills development, and making more money. These are the benefits of employment that every person has a right to and should care about — not just a specific, arbitrarily-chosen subsection of people born between a certain time period like Millennials or Sagittariusses. (Sagittarii? Sagitarians?)

But we also can’t forget that we live in a system of Catch-22s — train your workforce well and they might leave for a bigger paycheck; guaranteed pensions are unpopular with shareholders and investors; offer more money, and someone else will counter. But one thing is for sure: organizations that only provide people with a basic paycheck are at a disadvantage versus those companies that go beyond.

_________________________________________________________

About the Author

This article was written by Hyon S Chu. Hyon is a data scientist at Culture Amp — where we conduct analytics and research with data that comes from real people at companies like yours. Reach out to join the conversation.