Key Takeaway:

J.P. Morgan saved the financial system in 1907 by pledging $8 million to the next domino, the Trust Company of America, and convincing a dozen other banks and the U.S. Treasury to deposit $70 million into other vulnerable banks. Bank of America is backed by a safety net of federal agencies, such as the Treasury, the Fed, and the FDIC, due to J.P. Morgan’s opportunism in the aftermath of the 1907 panic. Venture capitalists panicked and withdrew $42 billion from SVB, leading to the FDIC seizing the bank due to mismatched durations and poor risk management. Venture capitalists worked behind the scenes to prevent the collapse of SVB, while big banks are depositing $30 billion in First Republic. The most important idea is that the FDIC and the U.S. Government are the only ones who can backstop depositors in times of crisis, and that the Venture Catastrophists are the other guys.

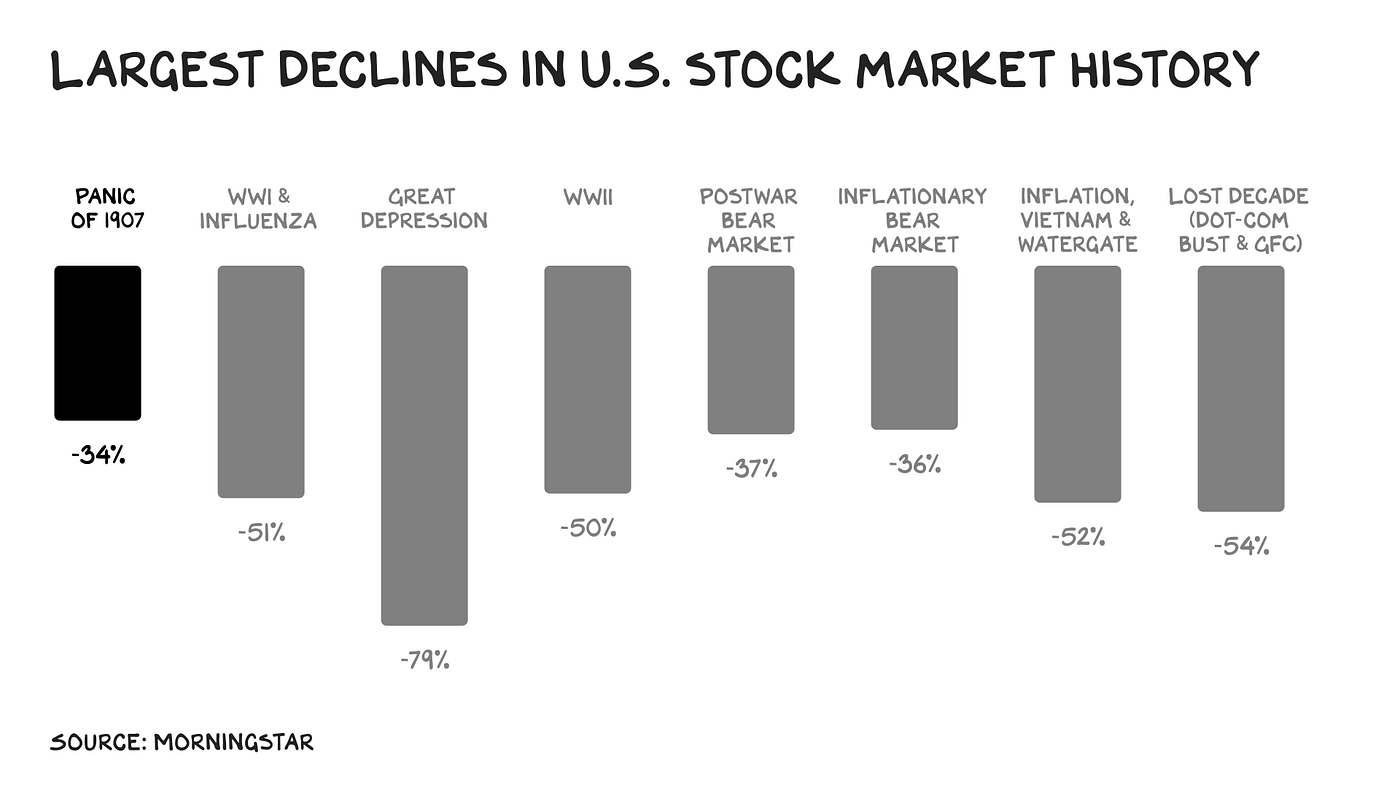

In 1907, amidst rising interest rates and a declining stock market, two New York bankers attempted to corner the stock of a copper company. Their scheme collapsed, and depositors at the banks that backed them pulled their money. One bank, Knickerbocker Trust, lacked the capital to withstand the bank run and, four days later, shut down. The rout was on.

J.P. Morgan, the nation’s preeminent banker and business leader, saw obligation and opportunity. He gathered the heads of New York’s banks at his Madison Avenue mansion and, the story goes, locked the doors and pocketed the key. “This is the place,” Morgan proclaimed, “to stop the trouble.” First he addressed his obligation: to save the system in which he’d built his wealth. He pledged an $8 million loan ($255 million in today’s dollars) to the next domino after Knickerbocker, the Trust Company of America. Then he convinced a dozen other banks and the U.S. Treasury to deposit $70 million into other vulnerable banks. The “Panic of 1907” subsided. Morgan saved the financial system. Fourteen years earlier, he’d done the same thing.

Trust

What J.P. Morgan understood was that banking, and by extension the economy, is not built on gold, labor, machinery, or spreadsheets, but on trust. Trust that deposits will be there when needed. That trust ruptured when the Knickerbocker Trust Company said, “We can’t.” Trust was restored when J.P. Morgan said, “We’ll ensure they can.” Once people trusted the banks again, the monetary crisis was solved. Fast forward to today: Can you imagine any part-time libertarian billionaire in the Valley pledging 5%, much less 50%, of their wealth to cauterize an emerging banking crisis?

Banks need your trust because they don’t actually have your money. When you deposit cash at the bank, it loans it to someone else. In fact, banks loan out more than they take in. It is a miracle and the cornerstone of our economy — turning short-term deposits into long-term loans. This is a good thing: Money sitting dormant does not fund startups, expand existing companies, or encourage consumers to … consume. It’s not useful.

Every bank is vulnerable to a run if enough people ask for their money on the same day. If Bank of America’s 67 million customers simultaneously withdrew their funds, in the same day/week/month, it would fail.

Together

But Bank of America doesn’t stand alone. It’s backed by a safety net of federal agencies — the Treasury, the Fed, the FDIC. Regulators, risk managers, and bank management are supposed to calibrate a sufficient level of liquidity to prevent insolvency — to “stress test” the bank. The Fed serves as a lender of last resort to troubled banks. Regulation moderates risk but can’t eliminate it.

This federal backstop exists, in substantial part, because J.P. Morgan didn’t see just obligation back in 1907. He saw opportunity. In the aftermath of the panic, Morgan called in the loans he’d made and went shopping for distressed assets: He acquired six banks, including the Trust Company of America, a steamship line, and the second-largest steel company in America (he already owned the largest). By 1913 officers of J.P. Morgan & Co. sat on the board of 112 public companies, representing 80% of the public market capitalization in the country.

We learned two lessons from 1907. The first was that the banking system needs a backstop. The second was that we shouldn’t rely on billionaires to be that backstop. In 1913, Congress passed the Federal Reserve Act, which created the central bank as we know it today. (The FDIC came along in 1933.) It’s no coincidence that the generations that followed 1907 made historic investments in the collective strength of America, from Social Security to the G.I. Bill to the Interstate Highway System. They understood their obligation to be part of a broader solution and rest it on the shoulders of democracy.

However, prosperity has a poor memory. By the 1980s, Morgan’s obligation was forgotten, and his opportunism became our model. Reagan and Thatcher branded the new (old) era: “There is no such thing as society,” said the Iron Lady. “There are individual men and women, and there are families.” Reagan added: “Government is not the solution to our problem; government is the problem.” Libertarianism, the political philosophy of a 19-year-old who’s just discovered Ayn Rand, became the governing ethos. Regulators were no longer backstops but impediments to be defunded or ignored.

By the 2010s, trust itself was seen as an inefficiency. Crypto rose to prominence with the core promise of “trustless transactions.” There’s no such thing.

SVB

Last week, Santa Clara had its own Knickerbocker moment. As the name suggests, Silicon Valley Bank was the bank of choice for venture capitalists and their portfolio companies, holding funds for nearly half of U.S. venture-backed companies. On Wednesday, March 8, SVB announced it had sold securities at a loss and was trying to raise more cash. A small number of VCs panicked and encouraged their portfolio companies to pull their funds, and on Thursday they withdrew $42 billion — breaching SVB’s liquidity cushion. On Friday the FDIC seized the bank.

Any complex event has multiple causes. The direct cause here is obvious: Too many of the banks’ customers tried to withdraw too much cash at once. The proximate causes were numerous:

- SVB committed the same sins that bring down most financial firms: mismatched durations and poor risk management. It invested long in mortgage loans and Treasury bonds, and borrowed short from startups that needed cash to fund operations.

- SVB lobbied the Trump administration (successfully) to raise the asset limit for tighter regulation.

- Interest rates rose, at a historic rate, decreasing the value of its long-term investments.

- SVB bungled its communications and strategy of trying to plug the hole in its balance sheet by selling equity, triggering the run it was trying to prevent.

- SVB’s customer base of startups is uniquely twitchy: They have cash balances well over the FDIC insurance limit of $250,000, and they’re interconnected through a handful of VC firms, which increases the risk of a bank stampede.

By Friday morning it was over, and the feds had arrived to turn on the lights and close the bar. While they were working over the weekend to ring-fence the contagion and make SVB’s depositors whole, a new species of venture capitalist was born on Twitter: the Venture Catastrophist. The fear mongering’s stated intention was to drum up support for a federal bailout of SVB depositors — many of whom were the Catastrophists themselves.

There are no libertarians in foxholes.

After SVB

In the immediate aftermath, observers are doing what they do after a complex catastrophe — cherry-picking the proximate cause that suits their politics and priors. It wasn’t rising interest rates, poor risk management, the concentration of the depositor base, or Venture Catastrophists on social media. It was all of it.

A more interesting question: What could have prevented the collapse? What is obvious is there does not appear to be a J.P. Morgan figure in the Valley with the leadership, citizenship, and sense of sacrifice to cauterize a contagion. There was, however, a group of venture capitalists working behind the scenes, quietly with our leaders, to figure out a solution. No all caps, no posing for the algorithms — just responsible people working around the clock because they saw themselves as part of the solution. Several hundred VC firms signed a letter committing to keeping their business with SVB, intended to make the asset more attractive to an acquirer.

More interesting than who signed the letter was who didn’t. In sum, venture capital firms that have a vested interest in destabilizing the banking system and the dollar, via crypto investments, have morphed from Americans to agents of chaos. I believe Marc Andreesen or Peter Thiel could have stopped the run with one tweet. They chose not to. This week, on the other side of the country, big banks, including the one J.P. founded, are following in his footsteps, depositing $30 billion in First Republic, after close coordination with Treasury Secretary Yellen.

I am a founder, director, or investor at four firms that have approximately $20 million in deposits at SVB. We did not pull out a dollar. (Note: One of the companies tried on Friday and was unsuccessful.) We didn’t keep our deposits at SVB because we’re moral or felt an obligation to save the bank, but because I went to the FDIC site and found that 73 banks have failed in the last 10 years, and all had their deposits backstopped. I didn’t lose a minute of sleep. Why?

- My backers, and the backers of the firms I’m an investor in, assured us they’d do whatever was required to make payroll, etc.; and

- Nothing is ever as good or as bad as it seems.

“This Is the Place”

It’s no surprise a community of increasingly atomized individuals chose survivalism over citizenship. Now, many Americans are disgusted with the backstopping, despite it being standard operating procedure, as they are wary of bailouts. More specifically, they are exhausted by a tech community that captures the upsides of risk but expects other Americans to bear the inevitable downsides.

Thanks to its ubiquitous apps — which create billions for management and investors but addict and depress our teens and make our discourse more coarse — the brand “Silicon Valley” has fallen farther faster than any brand other than “Musk.” If the failed bank had been “First Bank of Iowa Agriculture,” there would have been no reticence by the feds or public to backstop its depositors. Fortunately, the wisdom of prior generations to establish the FDIC and the steady hand of the U.S. Government has endured.

It comes down to this. What type of leader, business person, and (quite frankly) man do you want to be? When shit gets real, do you want to be the steady hand who stays calm and works with others, with purpose and skill, to figure out a solution? Or are you in the foxhole screaming, only giving your position away and making things worse? The real man here, the real American, is in Washington, and his name is Janet Yellen. The Venture Catastrophists are the other guys.